library(quantmod)

library(ggplot2)

library(xts)

library(highcharter)

library(PerformanceAnalytics)

library(dygraphs)Detailed stock analysis process.

## Dates have been loaded as a factor instead of as dates.

#There is need to convert this variable to the date class and covert the rest of the variables to xts(Extensible Time Series)

temp <- xts(x =fundreturn[,-1], order.by = as.Date(fundreturn[,1]))

# all the variables except data are coerced to xts using date as the index.

# Overwriting the fundreturn object with the xts temp object

fundreturn <- temp

str(fundreturn)An 'xts' object on 2007-06-01/2016-11-01 containing:

Data: num [1:114, 1:18] 0.024 0.0057 0.0165 0.0126 -0.0301 0.0026 0.0045 0.0218 0.027 0.0315 ...

- attr(*, "dimnames")=List of 2

..$ : NULL

..$ : chr [1:18] "SPY" "IJS" "VTI" "IYR" ...

Indexed by objects of class: [Date] TZ: UTC

xts Attributes:

NULLrm(temp) # getting rid of temp object

## Next I, stack variables of the same unique class within the same column.

#That is the returns of all the stocks in one column and the tickers in another column, indexed by the date variable.

# make use of a temporary object.

temp <- data.frame(index(fundreturn),

stack(as.data.frame(coredata(fundreturn))))

fundreturn_final <- temp# Give the variables more descriptive names

names(fundreturn_final)[1] <- "Year"

names(fundreturn_final)[2] <- "PercentageReturn"

names(fundreturn_final)[3] <- "Stockticker"

names(fundreturn_final)[1] "Year" "PercentageReturn" "Stockticker" rm(temp) # removing the temp. object

# we coerce the data frame back to xts to be able to use quantmod and highcharter

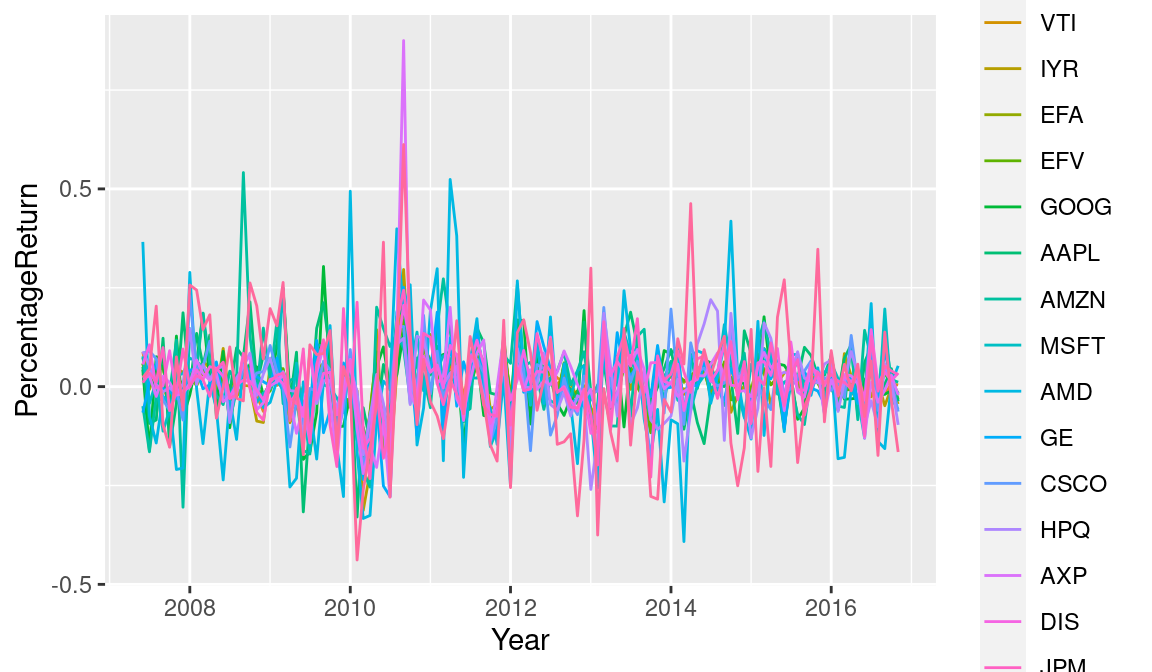

#fundreturn_final <- xts(x=fundreturn_final[-1], order.by = as.Date(fundreturn_final[,1]))ggplot(data = fundreturn_final, aes(x=Year,

y=PercentageReturn, color=Stockticker)) +

geom_line()

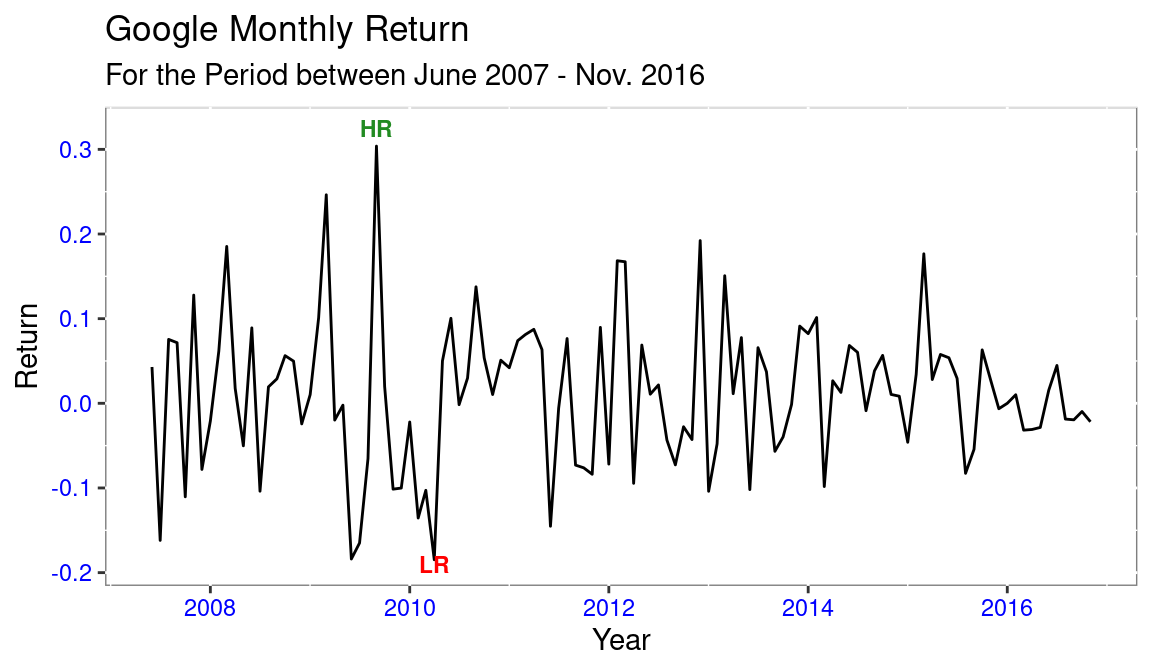

# Google stock Performance

# GOOG

GOOG <- subset(fundreturn_final, Stockticker=="GOOG")

g <- ggplot(data = GOOG, aes(x=Year, y=PercentageReturn)) +

geom_line()

# add features

g <- g + ggtitle("Google Monthly Return",

subtitle = "For the Period between June 2007 - Nov. 2016") +

theme(panel.background = element_rect(fill = "white",

colour = "grey50"),

axis.text = element_text(colour = "blue"),

axis.title.y = element_text(size = rel(1.0), angle = 90),

axis.title.x = element_text(size = rel(1.0), angle = 360))

g <- g + labs(x = "Year",

y ="Return")

g + annotate("text",x=as.Date("2009-09-01"),

y=0.3245,label="HR",

fontface="bold",size=3,

colour = "forestgreen") +

annotate("text",x=as.Date("2010-04-01"),

y=-0.1900,label="LR",

fontface="bold",size=3,

colour ="red")

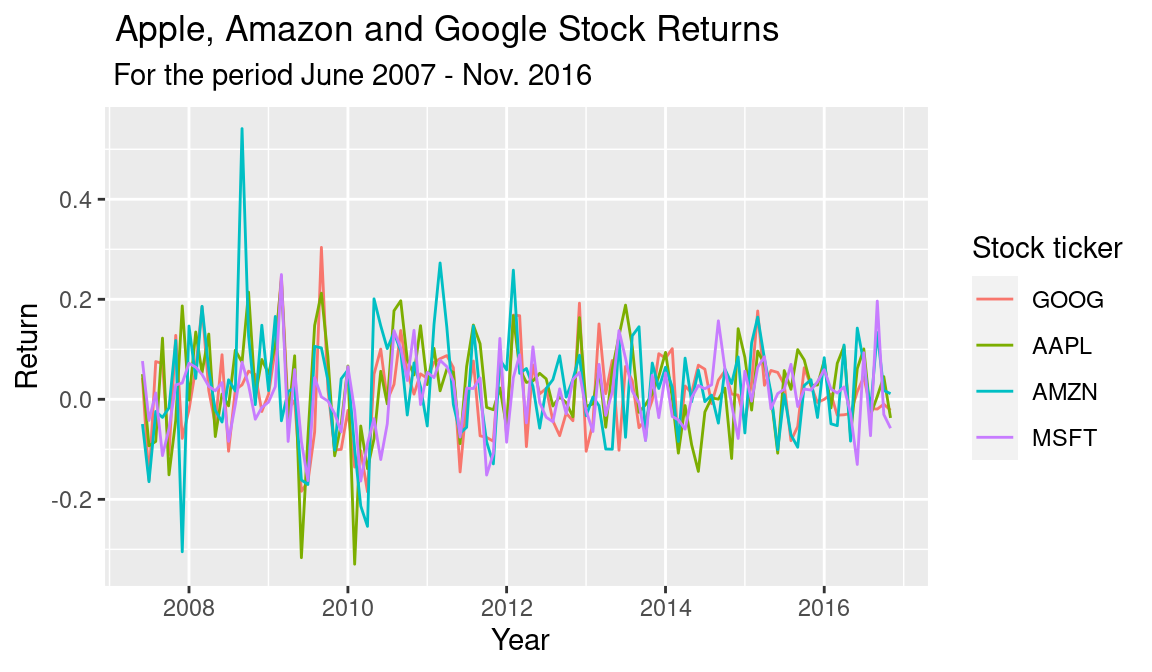

# Portfolio Performance Appraisal

# Having the following portfolio

# Google = GOOG, Amazon = AZMN,Apple = AAPL JP Morgans = JPM, Microsoft = MSFT, General Electric = GE, and Hewlett Packard = HPQ

#, "GE", "HPQ"

p1 <- subset(fundreturn_final, Stockticker =="AMZN")

p2 <- subset(fundreturn_final, Stockticker =="MSFT")

p3 <- subset(fundreturn_final, Stockticker =="AAPL")

p4 <- subset(fundreturn_final, Stockticker =="GOOG")

portfolio <- rbind(p1,p2,p3,p4) # binding the returns into one returns variable

rm("p1","p2", "p3","p4") # Removal of the temp. subsets

# quick visual representation of the data

p <- ggplot(data = portfolio, aes(x = Year, y =PercentageReturn, colour = Stockticker))+geom_line()

p + labs(

x = " Year",

y = "Return",

colour = "Stock ticker") +

ggtitle(" Apple, Amazon and Google Stock Returns",subtitle =" For the period June 2007 - Nov. 2016")

#Dygraphing

p1 <- subset(fundreturn_final, Stockticker =="AMZN")

p2 <- subset(fundreturn_final, Stockticker =="MSFT")

p3 <- subset(fundreturn_final, Stockticker =="AAPL")

p4 <- subset(fundreturn_final, Stockticker =="GOOG")

# Converting to xts before graphing

AMZN <- xts(x = p1[,c(-1,-3)], order.by = p1[,1])

MSFT <- xts(x = p2[,c(-1,-3)], order.by = p2[,1])

AAPL <- xts(x = p3[,c(-1,-3)], order.by = p3[,1])

GOOG_ <- xts(x = p4[,c(-1,-3)], order.by = p4[,1])

rm("p1","p2", "p3","p4") # Removal of the temp. subsets merged_returns <- merge.xts(AMZN,MSFT,AAPL,GOOG_) # merging the separate share returns into one xts object.

dygraph(merged_returns, main = "Amazon v Microsoft v Apple v Google") %>% # Using pipes to connect the codes

dyAxis("y", label ="Return") %>%

dyAxis("x", label ="Year") %>%

dyOptions(colors = RColorBrewer::brewer.pal(4, "Set2")) # Let's now evaluate the portfolio

## Part of the code is adapted from Jonathan Regenstein from RStudio

# We assume an equally weighted portfolio. Allocating 25% to all the stocks in our portfolio

w <- c(.25,.25,.25,.25)

# We use the performanceAnalytics built infuction Return.porftolio to calculate portfolio monthly returns

monthly_P_return <- Return.portfolio(R = merged_returns, weights = w)

# Use dygraphs to chart the portfolio monthly returns.

dygraph(monthly_P_return, main = "Portfolio Monthly Return") %>%

dyAxis("y", label = "Return")# Add the wealth.index = TRUE argument and, instead of returning monthly returns,

# the function will return the growth of $1 invested in the portfolio.

dollar_growth <- Return.portfolio(merged_returns, weights = w, wealth.index = TRUE)

# Use dygraphs to chart the growth of $1 in the portfolio.

dygraph(dollar_growth, main = "Growth of $1 Invested in Portfolio") %>%

dyAxis("y", label = "$")# Calculating the Sharpe Ratio

# Taking the US 10 Year Treasury Rate of 2.40% as the risk free rate.

# Making use of the built in SharpeRatio function in Performance Analytics package.

print(sharpe_ratio <- round(SharpeRatio(monthly_P_return, Rf = 0.024), 4)) portfolio.returns

StdDev Sharpe (Rf=2.4%, p=95%): -0.0634

VaR Sharpe (Rf=2.4%, p=95%): -0.0424

ES Sharpe (Rf=2.4%, p=95%): -0.0298Citation

BibTeX citation:

@online{simumba2017,

author = {Simumba, Aaron},

title = {Stocks {Portfolio} {Analysis}},

date = {2017-03-17},

url = {https://asimumba.rbind.io/blog/stock-returns/},

langid = {en}

}

For attribution, please cite this work as:

Simumba, Aaron. 2017. “Stocks Portfolio Analysis.” March

17, 2017. https://asimumba.rbind.io/blog/stock-returns/.